George IV - Results

The following are the results for George IV since January 2008 for two emini markets, ES and YM, for a single contract. The results include the whole of 2008 and several months of 2009. Since there are only about 6-7 trades a month in each market, it makes little sense to update the results more often than every third of a year, that is, every four months. This is so because one needs at least 30 trades to have a sensible even if still poor statistical sample that could give us a hint about the system performance free of statistical fluctuations.

The results assume a target of 6 points for ES (60 points for YM) and an initial stop-loss of 9 points (90 points for YM).

|

2008 ES: 51.5 pts - 65 trades YM: 355 pts - 66 trades |

|

2009 (through April)

ES: 39.75 pts - 32 trades

YM: 619 pts - 27 trades |

The good thing about using the 6/60 point target is that this lowers the slippage per trade as most (60%+) trades carry no slippage at all. Let's do a simple calculation to estimate the slippage in a case like that assuming a 2 tick slippage in ES on the trades that do not hit 6/60 point target and that there are 40% of them, for simplicity. Here is the average slippage in ES in ticks in a case like that: (6*0+4*2)/10=0.8. In YM, we get (6*0+4*3)/10=1.2. Thus the slippage per trade gets lowered by ca $15 and ca $9 per trade in ES and YM, correspondingly compared to the slippage in a system that closes its position with a market order (2 ticks in ES or 3 ticks in YM), say at the close of the trading session.

Let us round these numbers up to 1 (ES) and 2 (YM) ticks, to make them even more conservative and add $5 in commissions to it, which gives us $17.5 and $15 to subtract from the gross profit per trade. Over the period from January 2008 through April 2009 this profit turns out to be 91.25*$50/97=$47.0 in ES and 974*$5/93=$52.3 in YM.

What we get after deducting the slippage and commission is the net profit per trade estimated quite conservatively:

$29.5 in ES and $37.3 in YM.

These are very decent numbers for a simple emini daytrading system.

I stress the word "daytrading" to keep things in perspective as it is possible to have a better net profit per trade in swing systems that keep their positions open for several days, but this also increases your risk. However, for the sake of fair comparison, let me also add that there are daytrading systems out there that produce perhaps $5 in the net profit per trade, which needless to say is about breakeven.

I mention this in some detail as this site is also meant to educate traders and examples of calculations like that are often missing from other vendors' sites. And one good reason for that could be that calculations like that might reveal that the system is, well, about breakeven.

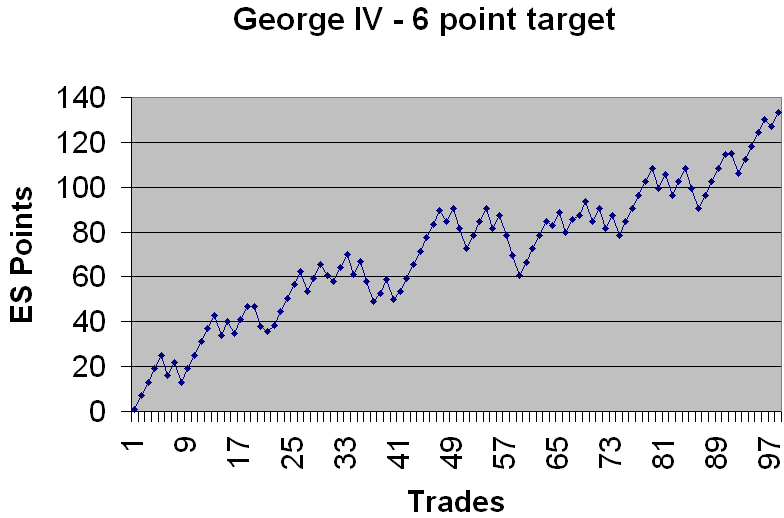

There are ways to make sure that your performance is even better. Start trading this system after 2 maximum losses in a row, although doing so after 3 consecutive losses that total 20 points or more (in ES) is even better.

That's what one of my clients did in February 2008. See how well he has done since then. See also how nicely looking his equity curve is.

{kind=link}

The system continues to do well. For more recent results, check out the notices section.